Buying property in Dubai starts with a single choice: which funding model will be best suited to my needs? Whether you use bank funding, a developer’s payment plan, or pay outright for your new home in Dubai, there are a lot of choices available to you in comparison to other international locations. When you’re able to understand the pros and cons of each funding model, you’ll have less to worry about and make your purchasing decisions with greater confidence.

Financing Guide in Dubai Real Estate

This guide to financing in Dubai will walk you through the process of choosing the right financing model for your Dubai real estate needs.

How do I Choose a Funding Model for My New Home in Dubai?

Most homebuyers in Dubai are faced with two main funding models: bank loans (mortgage) or developer funding plans. Based on their financial situation, location in Dubai and how much they wish to own, each model has its advantages and disadvantages. Some buyers want to ensure that they’ll have a stable income stream for years to come; other buyers want the ability to quickly exit the real estate market and find a new place to live. It’s essential that buyers understand how both funding routes operate so that they don’t waste time looking for homes outside of their means.

Bank Loans (Mortgages)

Bank loans (or mortgages) are the most popular financing model used by homebuyers in Dubai. Typically, residents can obtain a larger loan to value ratio than non-residents, and therefore, the amount of money they need to put into a down payment is lower. As well, most banks now offer fixed interest rates for the first couple of years of a mortgage, and then, the rate changes depending on the current state of the market. This structure allows buyers to anticipate their payments over the initial years of owning a home.

How Do Banks Determine Mortgage Eligibility and Approve Your Loan?

Before issuing a mortgage, banks look at an applicant’s income, past credit history, and outstanding debt obligations. To qualify for a mortgage in Dubai, salaried applicants will need to submit their latest salary certificate, bank statement and proof of employment. Self-employed applicants will need to submit audited financial statements and trade licenses to prove their income. For this reason, obtaining a mortgage pre-approval from a bank before starting your search for a home is highly advised. A mortgage pre-approval will enable you to determine a realistic price range for your search, and increase your negotiating position once you’ve found a home or entered into negotiations with a seller or developer.

Down Payment Requirements and Other Purchase Costs

A down payment is an important component of purchasing a home in Dubai. Typically, residents need to make a down payment of at least 20% of the home’s purchase price, while non-residents usually need to make a down payment of at least 40%. In addition to making a down payment, buyers should factor in additional costs associated with the purchase of a home in Dubai, including registration fees, valuation costs, and bank charges. If you prepare for these costs ahead of time, you’ll be able to avoid unnecessary delays during the transfer process.

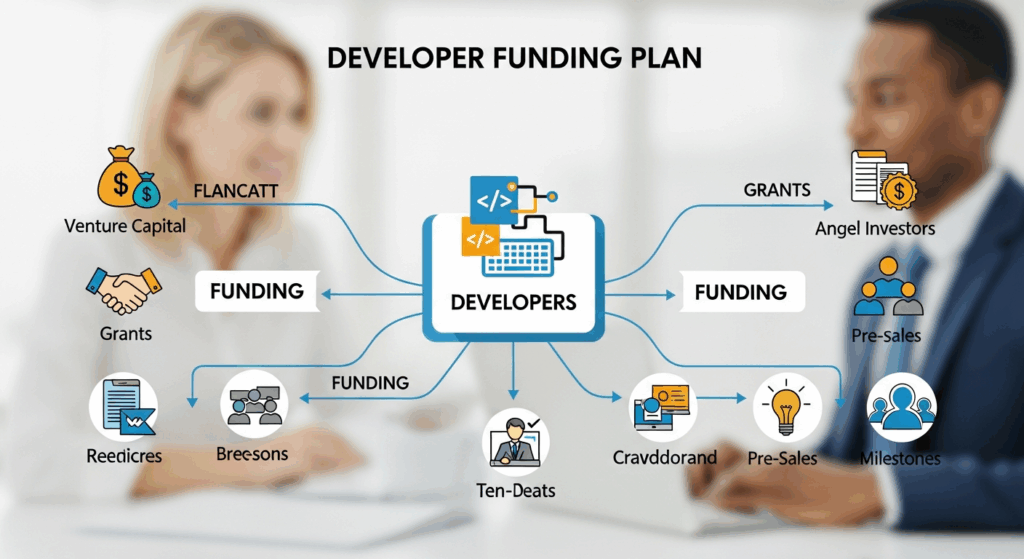

What is a Developer Funding Plan?

Developer funding plans are another financing model that is commonly used in Dubai, particularly when it comes to purchasing off-plan properties. Developers’ payment plans permit buyers to make payments for their home in stages, based on specific milestones in the construction of the project. In some instances, developers offer post-handover payment plans to buyers, allowing them to pay for their home over a longer period of time, after the completion of the building and after they have moved in. This approach enables buyers to manage their cash flow without having to rely on a bank loan to fund their purchase.

What are the Risks Involved with Using a Developer’s Funding Plan?

In addition to providing a high degree of flexibility for buyers, payment plans do involve risks. Buyers who use a developer’s funding plan need to carefully read the fine print on the contract to look for potential pitfalls. For example, if payments are made late, there may be penalty fees for the buyer or even a possible cancellation of the contract. Some developer funding plans also may have administration fees associated with them, but these may not always be clearly stated. As such, before signing any type of developer funding agreement, it is highly recommended for buyers to thoroughly review the payment terms so as to avoid any potential surprises during their time of home ownership.

Choosing Between a Bank Loan and a Developer Funding Plan

Ultimately, the decision about which is the best way to fund the purchase of your home in Dubai, depends upon what you are trying to accomplish long term and how much risk you want to take. If you like the predictability and the stability that comes with making regular, fixed monthly payments, then a bank loan (mortgage) would likely be the best choice for you. However, if you prefer the ability to buy into or out of the Dubai real estate market quickly and easily, then a developer funded plan would be the better choice. Additionally, many times, buyers may choose to take advantage of a combination of funding options by obtaining a mortgage from a bank after they receive title to their new home.

Finding Professional Guidance to Help You Make Smarter Financing Choices

Keyspace Realty

Keyspace Realty is here to assist you in navigating the complexities of funding your new home in Dubai by providing information on the various types of mortgage structures offered, the various payment plans offered by developers, and the overall cost of owning a home in Dubai. They can help you connect your financing choices to your personal life style and long-term objectives, ultimately reducing uncertainty and enabling you to make more confident decisions.

Keyspace Dubai

Keyspace Dubai is here to provide you with more comprehensive insights on the Dubai real estate market to help you compare multiple developments based on the various funding options available. By examining the developer payment plans and the criteria used by lenders to approve mortgage applications, Keyspace Dubai can help you to see how funding options impact the overall value of your purchase. This will enable you to compare your options based on more than just the purchase price.

How Will Market Conditions Impact Your Financing Decision?

The market conditions in Dubai can greatly affect your financing decision. Interest rates, developer incentives, and demand for housing can fluctuate throughout the year. As a result, some developers may create temporary payment plans, while lenders may change their mortgage interest rates due to the economic climate. Keeping yourself informed will allow you to take advantage of the market conditions that best support your financial objectives.

Planning for Your Exit Strategy Before You Even Buy

In conjunction with your financing decision, it is essential to think about your resale or rental plans for your home in Dubai. In Dubai, some developer payment plans limit resale until a certain percentage of the purchase price has been paid, while some mortgage agreements may impose early repayment penalties. Therefore, understanding these elements of your financing agreement will help you plan accordingly in case your circumstances change later.

Why Dubai Continues to Attract Buyers Seeking Financing Solutions

Dubai has established itself as a destination that is attractive to both end-users and investors alike due to the transparency of its regulatory environment and its protection of buyers. Dubai escrows funds for off-plan purchases and protects the registration process to ensure that owners’ rights are protected. These elements contribute to why Dubai remains a desirable destination for buyers seeking long-term security.

This financing guide to Dubai real estate demonstrates how understanding your financing options and the total costs involved can lead to smarter decisions regarding your property purchases. By knowing how to select a financing solution that fits your lifestyle and investment objectives, you can rest assured that you are making an informed decision regarding your next home purchase.

Frequently Asked Questions

What is the Minimum Salary Required to Obtain a Mortgage in Dubai?

Typically, the majority of banks in Dubai require a minimum monthly salary of approximately AED 15,000 to qualify for a mortgage, although the requirements differ between lenders.

Can Non-Residents Obtain a Mortgage in Dubai?

Yes, non-residents can apply for a mortgage in Dubai; however, non-residents usually require a larger down payment and meet stricter qualification standards.

Which Option Offers More Flexibility: Developer Payment Plans vs. Mortgages?

Payment plans offer greater flexibility than mortgages; however, the latter provides greater long-term stability. Ultimately, the best option will depend on your financial comfort and your desired outcome.

What Additional Costs Should Buyers Budget for?

Buyers should budget for registration fees, agent commissions, valuation costs, and bank fees.

Is Mortgage Pre-Approval Mandatory?

Pre-approval is not mandatory; however, it can aid you in determining a reasonable price range for your search, and strengthen your bargaining position once you locate a home or begin negotiations with a seller or developer.

NOTE: Pictures used in the advertisement are for illustration purposes only.